Delta Township resident Liz Beal has long been frustrated by the growing number of local businesses and services that have adopted credit card surcharge fees.

“Inflation is affecting the middle class the most, so why are we dinging them on every little thing when we’re the ones out there spending? It’s a complex problem, and I definitely think consumers are getting the short end of the stick,” Beal said.

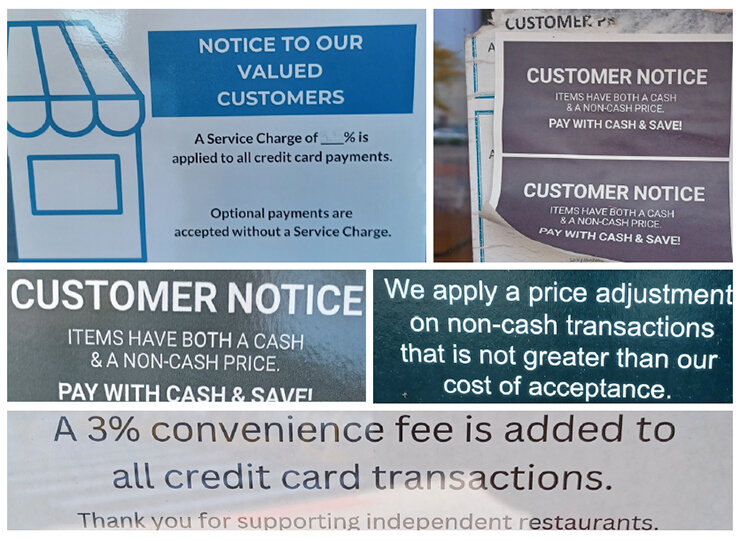

And they are getting it more and more often in Lansing. The trend toward credit card surcharges for consumer purchases began nationally a decade ago, but it seems to have hit Lansing with a heavy hand since the pandemic ended. More and more businesses, especially smaller, local establishments, are embracing it.

“I understand that it’s expensive for businesses to accept credit cards,” Beal, a real estate agent and former banker, said. However, it’s also a cost of doing business, especially when we’re moving into more of a cash-free society like we are.”

Businesses argue they are just trying to stay on top of inflation by passing along surcharges to cover what they pay in credit card fees.

Until 2013, merchants were prohibited from doing so. A 2005 antitrust class action lawsuit filed by nearly 12 million merchants against Visa and Mastercard opened the floodgates for a shift in that business model.

In 2013, Visa and Mastercard was ordered to pay merchants $7.25 billion in one of the largest antitrust settlements in U.S. history. By Jan. 27, 2013, merchants in Michigan were officially permitted to pass along a credit card surcharge of up to 4% of the purchase to offset fees. These fees average between 1.5% and 3%, but businesses are usually charged a flat fee for each transaction as well.

“Many businesses decided that it was time for them to not pay all those fees. Some have decided to pass along those costs to their shoppers. It’s something you’ve seen in bigger cities for a lot longer than you’ve seen around here,” Andrea Bitely, of the Michigan Retailers Association, said.

Bitely said this is especially the case with smaller, locally-owned restaurants and retailers that are more likely to operate on slim margins and may otherwise struggle to cover the fees without suffering a sizable loss.

“I think what it comes down to is that consumers need to be aware of these charges that businesses are putting onto cards, but at the same time understand that this is a business’s way of ensuring that they can pay to have products in their store, they can pay their employees, they can cover some of these growing costs that are associated with running and having a business,” Bitely said.

In an effort to provide an alternative, a growing number of local restaurants — including The Cosmos and Zoobies in Old Town, Dagwood’s Tavern and Eastside Fish Fry, Taste of Thai in East Lansing and The New Daily Bagel and Thai Village in Washington Square — offer discounts for cash payments.

“It’s growing,” Bitely said of the trend. “I think some people see it as a viable way to offer an alternativeD because it means they’re not processing something through their credit card system. It’s some savings for them, even if it’s just a small saving.”

Wan Wonnacott, manager at Taste of Thai, said that a 10% discount for cash purchases over $5 has been in place since the day she started working there over five years ago and estimates that nearly half of her customers will opt for cash transactions on any given day.

One business owner, who asked not to be identified because he didn’t see it as good business to promote surcharges at his establishment, said most of his customers are already aware of those fees. “Still, smacking them in the face with it is probably not necessarily the smartest idea,” he said.

“If you want that ease of use, you should probably either bring cash or you shouldn’t worry about how much you have to pay — or you can go to an ATM where they’re just going to charge you money anyways,” he said. “If our government wants to push a cashless society, that’s cool. But if you spend $5 at my store and I don’t charge you a fee, I lose money. If I go and use that at another store and they also lose money, then that $5 ends up being $2 or $3 real quick. On the other hand, my $5 worth of cash is still going to be worth $5 if I spend it correctly.”

Some consumers do understand that the extra charges aren’t padding the pockets of the businesses they patronize and are willing to pay a surcharge — provided the fees are transparently disclosed.

“If you want to give a discount for cash, I think that’s fine, and people would appreciate that,” Beal said. “I still think that there are a lot of benefits to using cash at small businesses, but I don’t like to be thinking I’m going to pay one price and, because I want to use a card, it’s going to be more.”

Rich Weingartner, a local computer analyst and Okemos resident, agreed. “They’re just going to have to advertise it correctly. If you see something advertised for $100, you should pay $100,” he said.

Connecticut, Massachusetts and Puerto Rico are the only U.S. states or territories that ban surcharges. Eight others — California, Florida, Kansas, Maine, New York, Oklahoma, Texas and Utah — still have anti-surcharge legislation on the books that are no longer enforceable due to recent court decisions. Michigan has no laws in place banning the practice, so long as fees are under the national 4% standard.

In Michigan, brick-and-mortar sellers who choose to implement a surcharge are required to post notices at the entrance and point of sale indicating that a fee will apply to credit card purchases while also itemizing the exact amount of the surcharge on sales receipts. Since 2017, gas station vendors have also been required by law to display any credit card surcharge fees next to the advertised fuel price on road signs in identical lettering at least half the size of the sale price.

Online retailers and third-party web payment systems have proven to be more resistant to regulation, however. Even the State of Michigan adds a surcharge at a rate of 2.35% for credit cards and a flat rate of $3.95 for debit cards on all digital payments. Similarly, beginning Oct. 1, Consumers Energy will start charging residential customers an additional flat fee of $2.99 to pay bills with a credit or debit card. The company expects the change to impact nearly 300,000 of its 2 million customers.

“Like many companies, we are encouraging customers to use payment methods that don’t incur fees — those fees ultimately are passed on to all customers. This step is one more we’re taking to help reduce the cost of energy for all customers. More than two-thirds of all energy providers take this approach, as do businesses of all types. Ultimately, this is good for all customers as we strive to keep bills low,” Consumers spokesperson Tracy Wimmer said.

Weingartner, who recently discovered his enrollment in autopay with Consumers had been eliminated altogether because of this change, said he still has “a little bit of hope” that legislators can come to the table and work together to address his concerns sooner rather than later.

“What they’re aiming for is not necessarily to get rid of the fees, but to make them transparent. From what I understand, there are at least glimmers of bipartisan support,” he said. “It’s a great start to have officials on both sides agreeing that ‘Yes, this is an issue.’ Now, is it a big enough issue that it will be given all the time it needs to go through hearings and votes? That remains to be seen.”

— TYLER SCHNEIDER

Support City Pulse - Donate Today!

Comments

No comments on this item Please log in to comment by clicking here